Should I Sell My House This Year?

If one of the questions you’re asking yourself today is, “Should I sell my house this year?” the current Housing Opportunities and Market Experience (HOME) Survey from the National Association of Realtors® (NAR) should boost your confidence as it relates to the current selling sentiment in the housing market. Even with all the information overload in the media circling around talk of a possible recession, the upcoming 2020 election, and more, Americans feel good about selling a house now. That’s some news to get excited about!

As the graph below shows, as of Q4 2019, 75% of people surveyed indicate they believe now is a good time to sell a home: In the case of those with a yearly salary of $100,000 or more, the results jumped even higher, coming in at an 82% positive sentiment.

In the case of those with a yearly salary of $100,000 or more, the results jumped even higher, coming in at an 82% positive sentiment.

When the study divided the outcomes by region, the results still consistently showed Americans feeling good about selling:

- Northeast: 71% positive

- Midwest: 76% positive

- South: 72% positive

- West: 81% positive

In addition to looking at income and region, the report also divided the results by generation, as shown in the graph below: As you can see, many believe that, despite everything going on in the world, it is still a good time to sell a home.

As you can see, many believe that, despite everything going on in the world, it is still a good time to sell a home.

According to NAR, the unsold inventory available today “sits at a 3.0-month supply at the current sales pace,” which is down from a 3.7-month supply in November. The current inventory is half of what we need for a normal or neutral housing market, which should have a 6.0-month supply of unsold inventory. This is good news for sellers, as Lawrence Yun, Chief Economist at NAR, says:

“Home sellers are positioned well, but prospective buyers aren’t as fortunate. Low inventory remains a problem, with first-time buyers affected the most.”

Bottom Line

If you’re ready to list your home, you can feel good about the current sentiment in the market. Let’s get together today to determine the best next step when it comes to selling your house this year.

Powered by WPeMatico

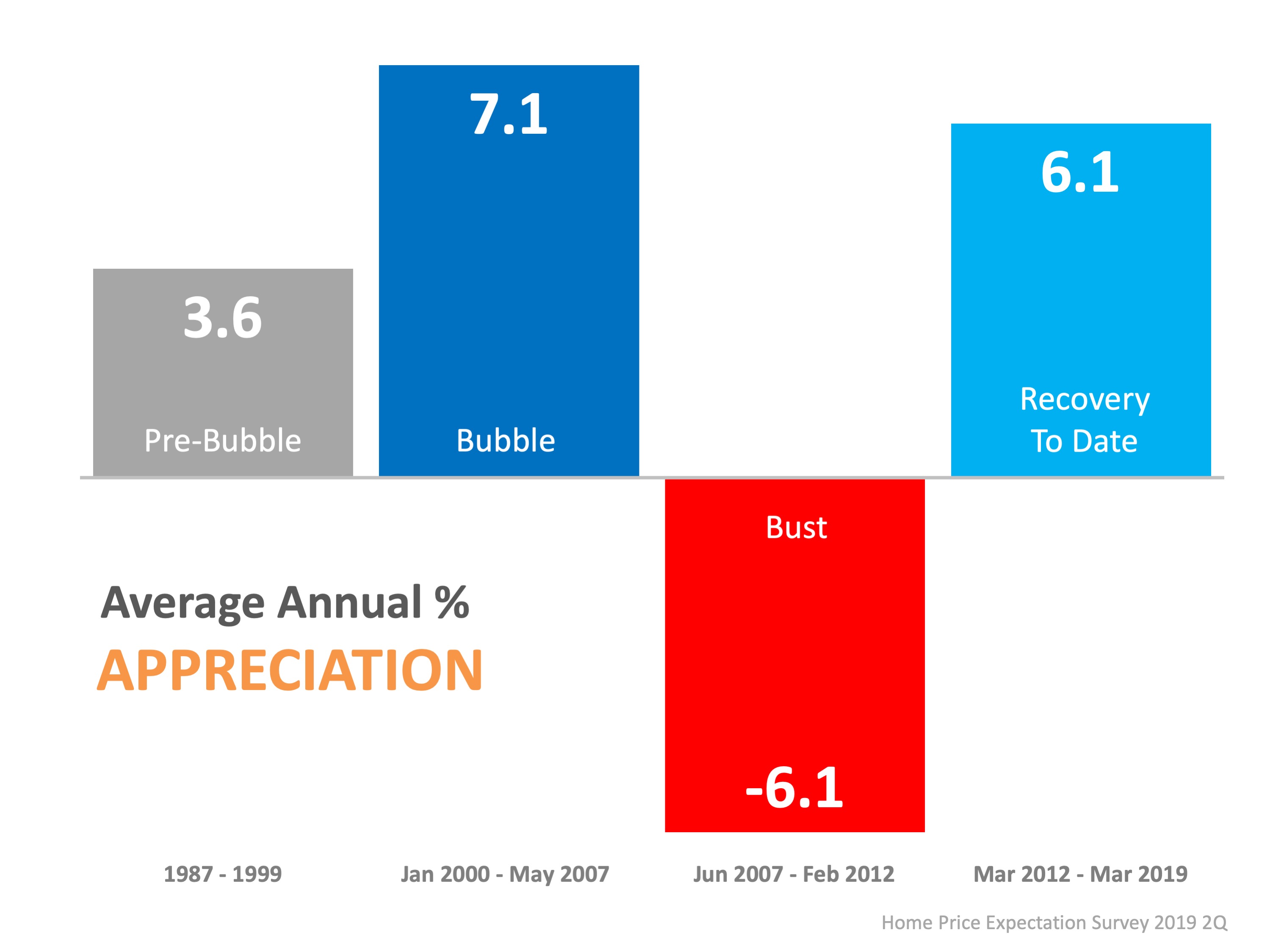

![A Recession Does Not Equal a Housing Crisis [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/08/29062756/2019830-Share-KCM-549x300.jpg)

![A Recession Does Not Equal a Housing Crisis [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/08/29061711/20190830-MEM.jpg)