The residential real estate market has come roaring out of the gates in 2020. Compared to this time last year, the number of buyers looking for a home is up 20%, and the number of home sales is up almost 10%. The increase in purchasing activity has caused home price appreciation to begin reaccelerating. Many analysts have boosted their projections for price appreciation this year.

Whenever home prices begin to increase, there’s an immediate concern about how that will impact the ability Americans have to purchase a home. That thinking is understandable. We must, however, realize that price is not the only element to the affordability equation. Mark Fleming, Chief Economist at First American, recently explained:

“When demand increases for a scarce (limited or low supply) good, prices will rise faster. The difference between houses and other goods is that we buy them with a mortgage. So, it’s not the actual price that matters, but the price relative to purchasing power.”

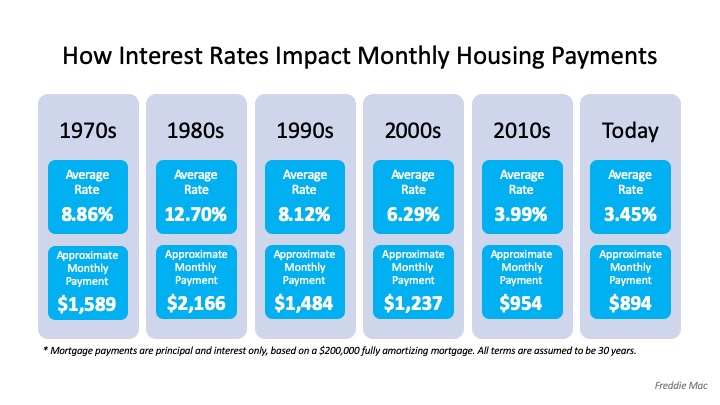

While home prices have risen recently, mortgage interest rates have fallen rather dramatically. At the beginning of last year, the 30-year fixed-rate mortgage stood at 4.46%. Today, that number stands over a full percentage point lower.

How does a lower mortgage rate impact your monthly mortgage payment?

Michael Hyman, a research data specialist for the National Association of Realtors (NAR), explained in a recent report that, even though home values have increased over the last year, the monthly cost of owning a home has decreased:

“With lower mortgage rates compared to one year ago, the payment as a percentage of income fell to 15.5%…from 17.1% a year ago.”

When purchasing a home, the price is not as important as its cost. Today, the monthly expense (cost) of purchasing the same house you could have purchased last year would be less. Or, you could purchase a more expensive home for the same monthly expense.

Fleming, looking at all aspects of the affordability equation (prices, wages, and mortgage rates), calculated the actual numbers in a recent blog post:

“Low mortgage rates and income growth triggered a 13.5% increase in house-buying power compared with a year ago.”

Since wages have increased and mortgage rates have dropped to historically low levels, this is a great time to buy your first home or move up to the home of your dreams. As Tendayi Kapfidze, Chief Economist at LendingTree, recently advised:

“If you are in a point in your life where you’re considering buying a home today, it’s a better time to buy than 10 years ago. If you can get a mortgage, you’re getting much lower interest rates, and it enables you to afford more.”

Bottom Line

Whether you’ve considered becoming a homeowner for the first time or have decided to sell your home and buy one that better suits your current lifestyle, now is a great time to get together and discuss your options.

![How Technology is Helping Buyers Navigate the Home Search Process [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/04/16173047/20200417-KCM-Share-549x300.jpg)

![How Technology is Helping Buyers Navigate the Home Search Process [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/04/16173049/20200417-MEM-Eng.png)

![What You Can Do to Keep Your Dream of Homeownership Moving Forward [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/03/26154454/20200327-KCM-Share-549x300.jpg)

![What You Can Do to Keep Your Dream of Homeownership Moving Forward [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/03/26154451/20200327-MEM-EN.jpg)