Big Demand for Small Homes

Movies, tv shows, and celebrities often have us dreaming of owning large homes, but the reality for most people is quite different.

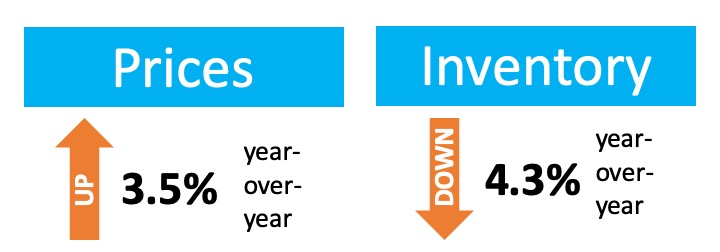

Since 2015, the square footage of newly built houses has been shrinking, according to Yahoo Finances. This is not projected to change as we continue into the beginning of the year.

“We expect this downsizing trend to continue in 2020, driven by a confluence of economic and demographic trends.”

Why are smaller homes trending now?

As noted in the article, there are a few main reasons for this demand:

- “Many of today’s younger, millennial home buyers have expressed a preference for denser, more urban homes that are more walkable to shared amenities.”

- “Today’s older homeowners are expressing a desire for smaller, less maintenance-heavy and more accessible (read: less stairs) homes as they age and move into newer homes.”

With these two demographic groups surging through the market, the demand for this type of home is rising. If you’re a homeowner with a smaller-scale house, now may be a great time to sell, as the demand for this end of the market is surely on the rise.

Bottom Line

The demand for smaller houses will continue to rise throughout 2020. Let’s get together to discuss what the housing inventory looks like in your neighborhood. It might be time for you to take advantage of this trend!

Powered by WPeMatico

![Working with a Local Real Estate Professional Makes All the Difference [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/12/19134136/20191227-Image-450x300.jpg)

![Working with a Local Real Estate Professional Makes All the Difference [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/12/19134109/20191227-MEM.jpg)